|

|

|

|

Monday, February 29, 2016

Friday, February 26, 2016

Here’s How Electric Cars Will Cause the Next Oil Crisis (BusinessWeek)

A shift is under way that will lead to widespread adoption of EVs in the next decade.

With all good technologies, there comes a time when buying the alternative no longer makes sense. Think smartphones in the past decade, color TVs in the 1970s, or even gasoline cars in the early 20th century. Predicting the timing of these shifts is difficult, but when it happens, the whole world changes.

It’s looking like the 2020s will be the decade of the electric car.

Battery prices fell 35 percent last year and are on a trajectory to make unsubsidized electric vehicles as affordable as their gasoline counterparts in the next six years, according to a new analysis of the electric-vehicle market by Bloomberg New Energy Finance (BNEF). That will be the start of a real mass-market liftoff for electric cars.

By 2040, long-range electric cars will cost less than $22,000 (in today’s dollars), according to the projections. Thirty-five percent of new cars worldwide will have a plug.

This isn’t something oil markets are planning for, and it’s easy to see why. Plug-in cars make up just one-tenth of 1 percent of the global car market today. They’re a rarity on the streets of most countries and still cost significantly more than similar gasoline burners. OPEC maintains that electric vehicles (EVs) will make up just 1 percent of cars in 2040. Last year ConocoPhillips Chief Executive Officer Ryan Lance told me EVs won’t have a material impact for another 50 years—probably not in his lifetime.

But here’s what we know: In the next few years, Tesla, Chevy, and Nissan plan to start selling long-range electric cars in the $30,000 range. Other carmakers and tech companies are investing billions on dozens of new models. By 2020, some of these will cost less and perform better than their gasoline counterparts. The aim would be to match the success of Tesla’s Model S, which now outsells its competitors in the large luxury class in the U.S. The question then is how much oil demand will these cars displace? And when will the reduced demand be enough to tip the scales and cause the next oil crisis?

First we need an estimate for how quickly sales will grow.

Last year EV sales grew by about 60 percent worldwide. That’s an interesting number, because it’s also roughly the annual growth rate that Tesla forecasts for sales through 2020, and it’s the same growth rate that helped the Ford Model T cruise past the horse and buggy in the 1910s. For comparison, solar panels are following a similar curve at around 50 percent growth each year, while LED light-bulb sales are soaring by about 140 percent each year.

Yesterday, on the first episode of Bloomberg’s new animated series Sooner Than You Think, we calculated the effect of continued 60 percent growth. We found that electric vehicles could displace oil demand of 2 million barrels a day as early as 2023. That would create a glut of oil equivalent to what triggered the 2014 oil crisis.

Compound annual growth rates as high as 60 percent can’t hold up for long, so it’s a very aggressive forecast. BNEF takes a more methodical approach in its analysis today, breaking down electric vehicles to their component costs to forecast when prices will drop enough to lure the average car buyer. Using BNEF’s model, we’ll cross the oil-crash benchmark of 2 million barrels a few years later—in 2028.

Predictions like these are tricky at best. The best one can hope for is to be more accurate than conventional wisdom, which in the oil industry is for little interest in electric cars going forward.

“If you look at reports like what OPEC puts out, what Exxon puts out, they put adoption at like 2 percent,” said Salim Morsy, BNEF analyst and author of today’s EV report. “Whether the end number by 2040 is 25 percent or 50 percent, it frankly doesn’t matter as much as making the binary call that there will be mass adoption.”

BNEF’s analysis focuses on the total cost of ownership of electric vehicles, including things like maintenance, gasoline costs, and—most important—the cost of batteries.

Batteries account for a third of the cost of building an electric car. For EVs to achieve widespread adoption, one of four things must happen:

1. Governments must offer incentives to lower the costs.

2. Manufacturers must accept extremely low profit margins.

3. Customers must be willing to pay more to drive electric.

4. The cost of batteries must come down.

The first three things are happening now in the early-adopter days of electric vehicles, but they can’t be sustained. Fortunately, the cost of batteries is headed in the right direction.

There’s another side to this EV equation: Where will all this electricity come from? By 2040, electric cars will draw 1,900 terawatt-hours of electricity, according to BNEF. That’s equivalent to 10 percent of humanity’s electricity produced last year.

The good news is electricity is getting cleaner. Since 2013, the world has been adding more electricity-generating capacity from wind and solar than from coal, natural gas, and oil combined. Electric cars will reduce the cost of battery storage and help store intermittent sun and wind power. In the move toward a cleaner grid, electric vehicles and renewable power create a mutually beneficial circle of demand.

And what about all the lithium and other finite materials used in the batteries? BNEF analyzed those markets as well, and found they’re just not an issue. Through 2030, battery packs will require less than 1 percent of the known reserves of lithium, nickel, manganese, and copper. They’ll require 4 percent of the world’s cobalt. After 2030, new battery chemistries will probably shift to other source materials, making packs lighter, smaller, and cheaper.

Despite all this, there’s still reason for oil markets to be skeptical. Manufacturers need to actually follow through on bringing down the price of electric cars, and there aren’t yet enough fast-charging stations for convenient long-distance travel. Many new drivers in China and India will continue to choose gasoline and diesel. Rising oil demand from developing countries could outweigh the impact of electric cars, especially if crude prices fall to $20 a barrel and stay there.

The other unknown that BNEF considers is the rise of autonomous cars and ride-sharing services like Uber and Lyft, which would all put more cars on the road that drive more than 20,000 miles a year. The more miles a car drives, the more economical battery packs become. If these new services are successful, they could boost electric-vehicle market share to 50 percent of new cars by 2040, according to BNEF.

One thing is certain: Whenever the oil crash comes, it will be only the beginning. Every year that follows will bring more electric cars to the road, and less demand for oil. Someone will be left holding the barrel.

The other unknown that BNEF considers is the rise of autonomous cars and ride-sharing services like Uber and Lyft, which would all put more cars on the road that drive more than 20,000 miles a year. The more miles a car drives, the more economical battery packs become. If these new services are successful, they could boost electric-vehicle market share to 50 percent of new cars by 2040, according to BNEF.

One thing is certain: Whenever the oil crash comes, it will be only the beginning. Every year that follows will bring more electric cars to the road, and less demand for oil. Someone will be left holding the barrel.

Thursday, February 25, 2016

Apple Calls on Congress to Form Committee for Privacy Issues (BusinessWeek)

- Apple Suits Up for Encryption Fight

- Surveys show public opinion backs unlocking terrorist's iPhone

- IPhone maker seeking to make case in public, outside of courts

Apple Inc. said the government should withdraw its court order requiring the company to help unlock a terrorist’s iPhone, and instead asked that U.S. lawmakers form an expert commission to discuss the implications for privacy, freedom and national security.

The company would “gladly participate” in such an effort, which has been suggested by some in Congress, Apple said in a statement on its website Monday.

Last week, U.S. Magistrate Judge Sheri Pym ordered Apple to lend “reasonable technical assistance” to the FBI in recovering information from the phone used by Syed Rizwan Farook, who killed 14 people in San Bernardino, California, with his wife in December. Apple has so far rejected the court order, saying that it would open a “Pandora’s Box” of privacy issues.

The standoff has ignited a long-simmering battle between the tech industry and the government, pitting concerns over civil liberties against the need for surveillance to fight terrorism. A Congressional panel would open the discussion to more voices than a court hearing would provide, and give the company a broader venue to make its case to the public, which is divided on the issue. According to a survey by the Pew Research Center, 51 percent of Americans are backing the FBI, while 38 percent say Apple shouldn’t unlock the phone.

“We feel the best way forward would be for the government to withdraw its demands under the All Writs Act and, as some in Congress have proposed, form a commission or other panel of experts on intelligence, technology, and civil liberties to discuss the implications for law enforcement, national security, privacy, and personal freedoms,” the company said Monday.

A Congressional commission also may pave the way for new laws dealing with questions of privacy and security, measures that technology companies like Apple and Microsoft Corp. say are needed because current communications laws predate technology such as cloud services and the Internet.

Security Feature

The case centers around whether the government can require Apple to write new software to compromise a key security feature of the company’s iOS mobile operating system. The government argues this is a one-time request that will aid an important terrorist investigation.

In a separate letter to employees on Monday, Apple Chief Executive Officer Tim Cook said the directive would create a dangerous precedent that could ultimately require the company to build software to help governments intercept private e-mails and access private health records.

On Sunday, FBI Director James Comey said the litigation over the phone “isn’t about trying to set a precedent or send any kind of message.”

“We don’t want to break anyone’s encryption or set a master key loose on the land,” Comey said in a letter on the agency’s website.“I hope folks will take a deep breath and stop saying the world is ending.”

Apple faces a Feb. 26 deadline to file its rebuttal to the government’s argument in court, with a hearing scheduled for March 22. Apple and FBI officials have been asked to testify in at least two congressional hearings. Meanwhile, the issue has become fodder among U.S. presidential candidates, with Republican front-runner Donald Trump calling for a ban on Apple products. The case could eventually reach the U.S. Supreme Court.

China's Huawei Backs Apple Stance in Phone Unlocking DisputeApple's New Lawyer Calls iPhone-Unlock Order a ‘Pandora's Box’

Wednesday, February 24, 2016

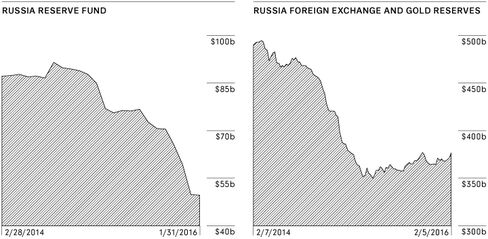

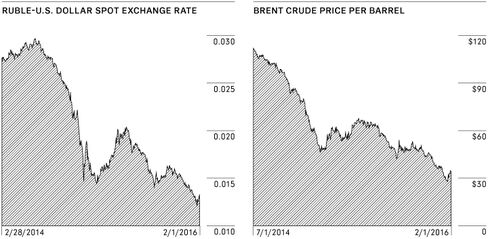

Can Things Get Any Worse for Russia? You're About to Find Out (BusinessWeek)

Investors who’ve made a fortune in the country say that with oil's plunge, the ruble's collapse, and Putin in power, all bets are off

For a decade, Dmitri Barinov has been following the volatile economy of his homeland from the safe distance of Union Investment’s offices in Frankfurt. Last year, as other money managers were steering clear of Russia’s broken economy, the Moscow-born Barinov pulled off something of a coup: He persuaded his bosses to take the plunge and buy Russian government bonds. It was a narrow bet, but he ended up winning because the central bank—after implementing the biggest interest rate hike since the Russian financial crisis in 1998 to prop up the collapsing ruble—changed course and aggressively backtracked. In the first 10 months of 2015, ruble-denominated government bonds handed investors such as Barinov a 25 percent return in dollar terms, the biggest gain for local bonds anywhere.

This year not even Barinov can spot an escape from the rubble of an economy mired in its longest recession in two decades. Sanctions imposed by the U.S. and the European Union to punish President Vladimir Putin for meddling in Ukraine remain a drag on growth. And oil’s decline to a 13-year low has been catastrophic for Russia, where almost 50 percent of government revenue comes from crude and natural gas. “With oil, you rely on a very volatile factor,” says Barinov, who oversees about $2.6 billion in assets. So as far as he’s concerned, “all bets are off.”

A persistent glut in crude supply could push prices to as low as $16 a barrel this year, according to former Russian Finance Minister Alexei Kudrin. Kudrin won plaudits overseas for his stewardship of Russia’s finances during Putin’s first decade in power. As the current crisis deepened, Bloomberg News reported in December, he was in discussions about a possible return to government. (He declined to comment on that.) A Putin ally, Kudrin remains negative about Russia’s prospects. “Over the next year to 18 months,” he says, “Russia will suffer major economic difficulties.”

Thanks to the plunge in oil prices, says Dmitri Barinov, "all bets are off" when it comes to investing in Russia.

In his early days in office, Putin didn’t have to contend with such unpleasantness. The year he came to power—2000—oil traded at an average of $28.44 a barrel. For eight years, he benefited from rising oil revenue and gross domestic product growth averaging 7 percent. Putin usually revels in his annual yearend press conference, fielding mostly harmless questions for hours on end. At the one on Dec. 17, however, even reporters from state-controlled media grilled him on the economy. Tamara Shornikova, a journalist from a state TV channel, asked the 63-year-old Putin how pensioners and others can get by when “bills keep growing.”

The president, his mood clearly darkening, noted disparagingly that the channel’s “audience is not very large, probably, but I sometimes watch your programs.” He said the government was trying to index pension increases to inflation (12.9 percent last year). “We will see how the situation in the Russian economy plays out,” he said. “I would really like 2016 indexation to be at least on par with the annual rate of inflation. I cannot say whether we will be able to do it or not.”

With the 2015 budget based on $50 a barrel, says former Deputy Economy Minister Mikhail Dmitriev, “even $40 a barrel is a dangerous scenario for Russia.” The country holds parliamentary polls in September and a presidential election in 2018, when Putin is expected to run again. The election cycle puts pressure on the government to spend beyond its means, says Dmitriev, who five years ago accurately foresaw the street demonstrations over allegations of vote rigging in legislative elections that turned into the biggest protests of Putin’s rule. “If social dissatisfaction boils over,” he says, “Russia will adopt a populist economic policy for an extended time.”

That kind of spending could exhaust Russia’s National Wellbeing and Reserve funds—currently totaling about $120 billion—within a year or two, says former Russian government adviser Sergei Guriev, who takes over as chief economist of the European Bank for Reconstruction and Development in mid-2016. “After that,” he says, “they will have to increase taxes on businesses, which will undermine incentives to invest, resulting in continuing capital outflow and a further decline in GDP.”

In mid-January, as snow blanketed Moscow, the mood was grim at the Gaidar Forum, a kind of Russia-focused mini-Davos. The yearly economic conference is named after the free-market Russian economist Yegor Gaidar, who pioneered the shock therapy that introduced capitalism to Russia in the early 1990s. Finance Minister Anton Siluanov set the tone for the event, warning that without deep budget cuts to keep the deficit at 3 percent, the country risks a financial crash like that of the late ’90s, when Russia defaulted on its debts, the ruble crashed, and inflation spun out of control.

Siluanov’s assessment surprised no one. Russian GDP contracted 3.7 percent last year and could fall as much as 3 percent in 2016 if oil prices average $35, according to the central bank. In January, the ruble sank to new depths—60 percent below its value against the dollar in mid-2014.

On a weekday evening in January at Moscow Domodedovo Airport, a trickle of passengers flowed through passport control, with half the booths closed. Several carriers, including Delta Air Lines, Air Berlin, and Cathay Pacific Airways, have stopped flying to Russia because of low passenger traffic and the ruble’s devaluation.

Last December, in the runup to New Year’s Eve and Orthodox Christmas festivities, retail sales—which fueled profits for the German cash-and-carry chain Metro, Sweden’s Ikea, and others during the boom years—had their biggest contraction since 1999. Not long ago, the Russian car market was set to overtake Germany’s, the largest in Europe. Yet in 2016, auto sales are expected to fall for a fourth consecutive year.

Putin has said Ukraine-related sanctions have helped devastate the Russian economy. He sees them as a conspiracy against Russian resurgence on the world scene. But the impact of sanctions pales in comparison with that of oil. In a recent report, Citigroup said sanctions are responsible for just one-tenth of Russia’s economic contraction, with plunging crude prices responsible for the rest.

Union Investment’s Barinov is hardly alone in scaling back investment in Russia. After also reaping profits from bond gains last year, Ogeday Topcular, managing partner at Ram Capital in Geneva, who helps oversee $300 million in fixed-income assets, sold all of his Russian local debt holdings in mid-2015 because of concern about the ruble’s dependence on oil. Mark Mobius, chairman of the emerging-markets group at Franklin Templeton Investments, which last year shut its underperforming 20-year-old Russia fund, says the oil curse is weighing heavily on the economy. “In view of the fact that the Russian government budget has been so reliant on oil prices, it is clear that the prospects for the economy and the market aren’t good,” he says.

Russia may exhaust its $120 billion in rainy-day funds within a year or two, says one former government adviser

Last fall, a glimmer of hope pierced the gloom. Russian assets rallied following the start of Putin’s air war in support of Syria’s President Bashar al-Assad in September. It was a clever-looking ploy by Putin, who has a knack for outflanking Western leaders. The idea was that Russian intervention would give Moscow a role in high-level diplomatic efforts to find a resolution to the Syrian civil war—and a seat at the top table of world powers once again.

If only temporarily, the gambit worked. Putin’s intervention forced U.S. and European leaders to engage in a conversation with Russia, fueling speculation that Ukraine-related sanctions might be eased. “Of course Putin wants to get out of isolation,” says Gleb Pavlovsky, a political analyst who advised the Kremlin during Putin’s first two terms. “The Syrian campaign was dreamed up precisely as a way to get out of isolation.”

At the end of last year, the U.S., Russia, and other big players agreed to push for a power-sharing government in Damascus by the middle of this year and elections a year later. In February they came up with a cease-fire plan. But the outcome of the peace process was in doubt as a Kremlin-backed military offensive not only shored up the Assad regime but also dangerously poisoned relations with Turkey, a NATO member and one of Russia’s biggest trading partners, which threatened to send troops to Syria.

Putin’s failure to diversify the economy away from its heavy dependence on oil remains the country’s fatal flaw. “The Russian government missed opportunities to implement serious reforms in the economy and diversify the budget revenues,” says Marco Ruijer, who oversees about $7 billion of debt as a money manager at NN Investment Partners in The Hague. While some Russian sovereign and corporate bonds are “attractive,” he says, “many investors are now selling everything that’s oil-related, and Russia is part of that, of course.”

Cayman Islands-based Prosperity Capital Management, which has $2 billion invested in the country, is a rare bull among bears. It’s counting on a rebound in oil prices and an improvement in the geopolitical climate. “The issue of sanctions has been pushed aside,” Prosperity director Ivan Mazalov says. “Investors are used to working with Russian assets in the new reality.” In this new reality, if there’s any ray of hope, it’s that the markets have already discounted Russia’s myriad problems, says John Manley, who helps oversee about $233 billion as chief equity strategist for Wells Fargo Funds Management in New York.

Putin could reassure investors by moving ahead with long-stalled privatization plans as well as improving the rule of law to ease pressure on businesses, says Ivan Tchakarov, chief economist in Russia for Citigroup. Russia ranked 119th on Berlin-based Transparency International’s corruption perception index, released in January, behind Pakistan and Tanzania.

Fundamentally, Russia is a “commodity play,” says Gary Greenberg, who helps oversee about $1.8 billion as head of emerging-markets equities at London-based fund manager Hermes Investment Management. Since Russia’s main exports—raw materials—are dependent directly and indirectly on China’s lackluster growth, the outlook for Russia “is moderate at best,” he says.

“In terms of emerging markets, it feels a lot like 1997,” says John-Paul Smith, the former Deutsche Bank strategist who predicted Russia’s 1998 market crash and went on to found Ecstrat, a London-based research firm. “The Chinese have been doing everything to get their economy going again, and they simply can’t do it.”

Then there’s the bleak view of Bill Browder, an American investor who became one of Putin’s most nettlesome bêtes noires and paid a price for it. Browder, a grandson of a U.S. Communist Party leader, ventured into Russia in the 1990s. He made a fortune specializing in undervalued Russian blue-chip stocks such as state-run Gazprom, the largest gas producer in the world, which saw the value of its stock soar 750 percent from 1999 to 2005. Browder’s Hermitage Capital Management started with $25 million in 1996 and at its 2005 peak had $4.5 billion under management, making it the biggest investment fund in Russia.

The London-based Browder was barred from Russia in 2005 after pushing aggressively for the rights of minority shareholders. He became a vocal critic of Putin after his accountant, Sergei Magnitsky, uncovered the theft of $230 million from the Russian treasury and later died under suspicious circumstances in a Moscow prison in 2009. For Browder, like many investors with long experience in Russia, it all comes down to Putin, who’s expected to win reelection to another six-year term in 2018, despite Russia’s economic travails. “No matter how cheap anything might seem,” Browder says, “it doesn’t matter if you’re on a negative trajectory.” He says the economy still has depths to plumb. “It hasn’t hit bottom, because Putin is still in power.”

Tuesday, February 23, 2016

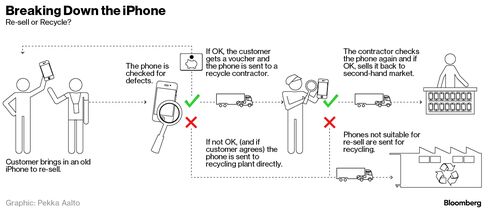

Where Your iPhone Goes to Die (and Be Reborn) (BusinessWeek)

At the end of their useful lives, many iPhones face the crusher.

At a dedicated factory with 24-hour security in an undisclosed location in Hong Kong, iPhones are being carefully and meticulously destroyed.

The plant is one of a handful around the world, chosen by Apple Inc. to grind up and recycle its iconic phones. And just as the companies that manufacture the handsets are subject to strict standards and secrecy, the same applies in reverse for their disassembly, right down to weighing the shreds, to make sure nothing is lost.

Apple has sold more than 570 million iPhones since that January morning nine years ago when Steve Jobs stepped on stage in San Francisco to “reinvent the phone.” Even Apple doesn’t know how many of those phones are still out there -- in the hands of their second, third or fourth owner, or sitting forgotten in a drawer. But the company wants to ensure as few as possible end up in landfills.

That’s the job of the plant in an industrial park in Hong Kong’s Yuen Long district belonging to Apple contractor Li Tong Group. This is where iPhones, iPads and iMacs come to die.

While global brands including HP, Huawei, Amazon and Microsoft also have detailed protocols for recycling their products, Apple’s are the most rigid and exacting, according to people involved in the processes, who declined to be identified because they’re not authorized to speak about clients.

"I think people expect it of us, I think our customers hold us to a high standard," Lisa Jackson, Apple’s head of environmental affairs, said by phone from the company’s Cupertino headquarters. "It’s difficult, because these are incredibly complex pieces of product."

Neither Apple nor Li Tong would provide access to the Hong Kong facility, say how many units it recycles, or give specifics of the de-manufacturing process.

In the electronics recycling business, the benchmark is to try to collect and recycle 70 percent, by weight, of the devices produced seven years earlier. Jackson says Apple exceeds that, typically reaching 85 percent, including recycling some non-Apple products that customers bring in.

That means it will have to get hold of and destroy the equivalent of more than 9 million of 2009’s iPhone 3GS models this year around the world. With iPhone sales climbing to 155 million units last fiscal year, grinding up Apple products is a growth business.

Closely held Li Tong, which also recycles equipment from other manufacturers, has three sites in Hong Kong and a dozen more worldwide. It expects global capacity to climb more than 20 percent this year, including a new facility in San Francisco.

Apple said it collected more than 40,000 tons of e-waste in 2014 from recycled devices, including enough steel to build 100 miles of railway track.

Brightstar Corp., based in Miami, Florida, TES-AMM in Singapore, Hong-Kong’s Li Tong and Foxconn Technology Group, the most famous manufacturer of iPhones, are part of a global network of recyclers that agreed to more than 50 rules, ranging from security, to insurance, to auditing, in the destruction of the phones.

The process starts at hundreds of Apple stores globally, or online, where the company offers gift certificates to lure iPhone owners to sell back their devices.

After a quick test, the recycler will either buy the phone or offer to scrap it for free. In the U.S., payouts for working phones range from $100 for the smallest-capacity iPhone 4, to $350 for the largest iPhone 6 Plus. More stringent testing then shows whether the handset can be resold or must be scrapped.

Apple’s U.S. recycler declined to comment while Terence Ng, director of South East Asian partner TES-AMM didn’t respond to e-mail and phone messages. Once Apple’s partners decide a phone must be scrapped, a deconstruction process begins that is remarkably similar to Apple’s production model, only in reverse.

Apple pays for the service and owns every gram, from the used phone at the start to the pile of dust at the end, said Linda Li, chief strategy officer for Li Tong. The journey, consisting of about 10 steps, is controlled, measured and scripted through vacuum-sealed rooms that are designed to capture 100 percent of the chemicals and gasses released during the process, she said.

Apple collected more than 40,000 tons of e-waste in 2014

Reclaimed iPhones can’t be shipped across regions, must have their storage wiped, and must have all logos removed. The scrap can’t be mixed with that of other brand names, so recyclers need to have dedicated facilities for Apple, Li said. Apple staff monitor the process at Li Tong’s factory which employs about 300 people.

While some brands salvage components such as chips that can be used to repair faulty phones, Apple has a full-destruction policy.

“Shredding components takes more energy than repurposing,” Li said. Li Tong works with other customers to advise on how to design products that are easier to deconstruct, taking cameras from smartphones for reuse in toy drones, and adapting screens from Microsoft Surface tablets to use in New York taxis, she said.

Apple shreds its devices to avoid having fake Apple products appearing on the secondary market, Jackson said. The company is working on ways to reuse components in the future, she said, declining to elaborate.

"There’s an e-waste problem in the world," she said. "If we really want to leave the world better than we found it, we have to invest in ways to go further than what happens now."

And once it’s ground into shreds, what becomes of your old iPhone? Hazardous waste is stored at a licensed facility and the recycling partners can take a commission on other extracted materials such as gold and copper. The rest is reincarnated as aluminum window frames and furniture, or glass tiles.

Monday, February 22, 2016

The Failure of Money to Buy the Presidential Nomination, in One Chart (BusinessWeek)

Some of the campaigns that are spending the most are also doing the worst.

Jeb Bush speaks during a campaign event in North Charleston, South Carolina, on Feb. 15, 2016.

The current U.S. presidential race is on pace to be the most expensive ever. Outside groups known as super-PACs are playing an unprecedented role, dominating the first few months of fundraising by collecting checks of $1 million or more from wealthy individuals. These groups raised about $348 million in 2015, compared with about $438 million gathered by the campaigns themselves, according to data from the Center for Responsive Politics.

What's all that money bought? For Jeb Bush, not much. His super-PAC's massive expenditures on TV ads have failed to stop a decline in the polls for the Republican nomination. Meanwhile, Donald Trump rocketed to the top by spending relatively little. In part, this was because Trump proved adept at generating free publicity.

We decided to chart the relationship, or lack thereof, between spending and success in the polls. For spending, we compiled Federal Election Commission data on how much each presidential campaign and presidential super-PAC spent through Dec. 31. (New data for January will be disclosed Feb. 20.) Then we looked at the change in position in the polls, based on the average poll ranking for each candidate as compiled by Pollster.com. We compared each candidate's position at the end of December to their rank as of June 29. Here's the result for each candidate who was still in the race as of Dec. 31:

If you thought more spending leads to better poll results, you might expect most of the candidates to form a line stretching from the bottom-left to upper-right corner. The reality is messier, and if anything, the line seems to point the other way. That might give pause to anyone considering writing the next $1 million check.

Wednesday, February 17, 2016

International Women's Day Luncheon - March 8, 2016

|

||||

|

||||

|

Tuesday, February 16, 2016

Friday, February 12, 2016

Boeing to Face SEC Probe of Dreamliner and 747 Accounting (BusinessWeek)

- Investigation said to review forecasts tied to costs and sales

- Regulator examining company's use of `program accounting'

The U.S. Securities and Exchange Commission is investigating whether Boeing Co. properly accounted for the costs and expected sales of two of its best known jetliners, according to people with knowledge of the matter.

The probe, which involves a whistleblower’s complaint, centers on projections Boeing made about the long-term profitability for the 787 Dreamliner and the 747 jumbo aircraft, said one of the people, who asked not to be named because the investigation isn’t public. Both planes are among Boeing’s most iconic, renowned for the technological advancements they introduced, as well as the development headaches they brought the company.

Underlying the SEC review is a financial reporting method known as program accounting that allows Boeing to spread the enormous upfront costs of manufacturing planes over many years. While the SEC has broadly blessed its use in the aerospace industry, critics have said the system can give too much leeway to smooth earnings and obscure potential losses.

“We typically do not comment on media inquiries of this nature,” Boeing spokesman Chaz Bickers said in an e-mailed statement. SEC spokesman John Nester declined to comment.

Share Drop

Boeing fell 6.8 percent to $108.44 in New York, the lowest closing price in more than two years.

SEC enforcement officials have yet to reach any conclusions and could decide against bringing a case, said the people. The issues involved are complex and there are few black-and-white rules governing how companies apply program accounting, one person said.

Program accounting has been around for decades. It was first championed by the aerospace industry to address the problem that companies’ biggest expenses are amassed upfront, as they design planes and devise manufacturing processes. Costs typically fall as the assembly becomes more efficient, making it cheaper to build the later jets than the earlier ones.

The method, which is fully compliant with Generally Accepted Accounting Principles, lets companies average out the costs and anticipated profits over the duration of the “program” for a specific jet, a period that can last decades and encompass hundreds or even thousands of aircraft.

The expected costs and sales are estimates and they must be updated -- and a loss recorded -- when the program is determined to have reached a point where earnings won’t catch up to losses.

Boeing’s Forecasts

As part of the investigation, SEC enforcement attorneys are examining whether Boeing’s financial statements relied on sales forecasts that might be too optimistic, one person said. Another avenue of inquiry is whether Boeing’s estimates for declining production costs will come to fruition, the person said.

A whistleblower has given SEC officials internal documents and data about Boeing’s accounting, according to the people. The tipster first raised concerns with the regulator more than a year ago, one person said. SEC policy is to not reveal the identities of whistleblowers.

Over the years, a handful of aerospace analysts have questioned whether Boeing will be able to recoup its costs for both the 787 and the latest 747, both of which debuted far behind schedule in 2011. In general, the company has enjoyed a good reputation on Wall Street, earning billions of dollars in annual profits and winning buy recommendations from most researchers who follow the industry.

Boeing’s accounting projects that the company will eventually make money on the Dreamliner despite already spending $28.5 billion on inventory and manufacturing. The forecast hinges on Boeing selling about 1,300 planes and assumes profits on its later deliveries will offset high costs stemming from early production snarls.

The SEC investigation “is potentially material and now a key focus for us,” Seth Seifman, an analyst at JPMorgan Chase & Co., said in a note to clients.

“If the issue here is whether Boeing should have already booked a 787 charge that many believe inevitable, that will be less damaging to the stock,” he said. “If there is any impact on our 787 cash flow forecasts for the coming years, this would be more significant.”

Plateauing Expenses

Boeing told investors during a January conference call that its Dreamliner expenses would plateau this year and then begin to decline as it speeds up production.

“We still have work ahead of us on the 787,” Boeing Chief Executive Officer Dennis Muilenburg said on the call. He added that the company is “focused on solid day-to-day execution and risk reduction, while improving long-term productivity and cash flow.”

Some analysts are skeptical that margins will improve enough to offset money that Boeing has already poured into the 787. Credit Suisse Group AG analyst Robert Spingarn estimated the company may face a $7.5 billion shortfall on the jet, according to a December report.

Boeing’s outlook for the latest and largest version of its jumbo family, known as the 747-8, has also been questioned by some aerospace analysts.

Accounting Losses

Over the years, Boeing has recorded several accounting losses, totaling $2.6 billion, for the 747-8 program. The most recent was last month when the company reported an after-tax loss of $569 million and announced it would halve its production to six jumbos a year.

Boeing’s current accounting estimates for the program’s profitability rely on it selling 35 more 747-8s.

Meeting those numbers could be a challenge. The company has only had 121 orders for the jet since 2005, and most of those sales came before the 2008 financial crisis. In addition, Boeing only netted two 747-8 sales over the previous two years. It ended up buying both planes itself as part of a lease-back deal with a Russian cargo company.

Boeing executives have said they are hopeful of a possible resurgence late this decade for the 747 freighter, whose size and cargo-loading capabilities are unmatched. The company’s other sales prospects for the 747 include replacements for the Air Force One aircraft that ferry U.S. presidents.

Jason Gursky, senior aerospace and defense analyst with Citigroup Inc., isn’t as optimistic.

“We expect the line to fully close early next decade after the Air Force One replacement,” Gursky wrote in a Jan. 22 report. He said the 747 order book is “very weak.”

Thursday, February 11, 2016

Imagine Google's VR gadget without the cardboard. Google does

Google's virtual reality ambitions leave cardboard behind.

The Web giant is planning to release a new VR headset later this year, the Financial Times reported Sunday. A successor to Google's Cardboard VR viewer released in 2014, the new smartphone-based headset would sport improved sensors and lenses housed in a solid plastic casing.

The move would underscore the continuing maturation of VR, which promises to transport goggle-wearing users to digitally created 3D worlds. It's all the rage among big tech companies: Facebook is on the verge of releasing its long-awaited Oculus Rift headset, while Sony, Samsung and HTC are also heavily invested in the technology.

Microsoft's HoloLens, meanwhile, is aimed at augmented reality, which adds 3D computer-generated scenes to people's view of the real world. Apple has also reportedly assembled a secret research group focused on virtual and augmented reality.

VR's potential extends well beyond the early emphasis on its use in video games, virtual field trips and reboots of classic toys. Backers say it could radically change the way we use computers, with ripple effects into how we communicate with one another.

Apple CEO Tim Cook last month summed up the fascination. "I don't think it's a niche," he said. "It's really cool. It has some interesting applications."

Whether consumers will bite, though, remains a mystery. Samsung has yet to reveal sales figures for its Gear VR headset, which was released last year for $99 (£80 in the UK or AU$159 in Australia), not including the price of a smartphone to power it. Other major devices, ranging from the $599 (£499 or AU$649) Oculus Rift to HTC's Vive to Sony's PlayStation VR are all expected to be released this year.

With Cardboard, Google took a bargain-basement tack. For $30 or less, consumers get a corrugated-paper housing for the smartphone they already own, with cutouts for nose and eyes. An app on the phone delivers the VR experience as cardboard blinders shut out the viewer's surroundings. Little more than a party favor, Google Cardboard could serve as a gateway drug to get people hooked on VR.

Google declined to comment for this story, but CEO Sundar Pichai last week signaled the Mountain View, California-based company's continued interest in virtual reality. He noted that more than 5 million Cardboard viewers have been shipped.

"It's still incredible early innings for virtual reality as a platform," Pichai said during an earnings conference call. "Cardboard is just a first step, but we are excited by the progress we have seen."

Tuesday, February 9, 2016

The Rich Are Already Using Robo-Advisers, and That Scares Banks (BusinessWeek)

- Are Robo-Advisers Better Than Humans?

- About 15% of Schwab's robo-clients have at least $1 million

- Morgan Stanley, Wells Fargo, BofA planning automated services

Banks are watching wealthy clients flirt with robo-advisers, and that’s one reason the lenders are racing to release their own versions of the automated investing technology this year, according to a consultant.

Millennials and small investors aren’t the only ones using robo-advisers, a group that includes pioneers Wealthfront Inc. and Betterment LLC and services provided by mutual-fund giants, said Kendra Thompson, an Accenture Plc managing director. At Charles Schwab Corp., about 15 percent of those in automated portfolios have at least $1 million at the company.

“It’s real money moving,” Thompson said in an interview. “You’re seeing experimentation from people with much larger portfolios, where they’re taking a portion of their money and putting them in these offerings to try them out.”

Traditional brokerages including Morgan Stanley, Bank of America Corp. and Wells Fargo & Co. are under pressure to justify the fees they charge as the low-cost services gain acceptance. The banks, which collectively employ about 46,000 human advisers, will respond by developing tools based on artificial intelligence for their employees, as well as self-service channels for customers, Thompson said.

“Now that they’re starting to see the money move, it’s not taking very long for them to connect the dots and say, ‘Whatever I offer for a fee better be better than what they’re offering for almost nothing,”’ Thompson said. Technology will “make advisers look smarter, better, stronger and more on top of the ball.”

Keeping Humans

Robo-advisers, which use computer programs to provide investment advice online, typically charge less than half the fees of traditional brokerages, which cost at least 1 percent of assets under management. The newer services will surge, managing as much as $2.2 trillion by 2020, according to consulting firm A.T. Kearney.

More than half of Betterment’s $3.3 billion of assets under management comes from people with more than $100,000 at the firm, according to spokeswoman Arielle Sobel. Wealthfront has more than a third of its almost $3 billion in assets in accounts requiring at least $100,000, said spokeswoman Kate Wauck. Schwab, one of the first established investment firms to produce an automated product, attracted $5.3 billion to its offering in its first nine months, according to spokesman Michael Cianfrocca.

Bank leaders including Morgan Stanley Chief Executive Officer James Gorman and Wells Fargo Chief Financial Officer John Shrewsberry have said their firms must develop robo-advisers to complement their sales force.

Customers want both the slick technology and the ability to speak to a person, especially in volatile markets like now, Jay Welker, president of Wells Fargo’s private bank, said in an interview.

“Robo is a positive disruptor,” Welker said. “We think of robo in terms of serving multi-generational families.”

Monday, February 8, 2016

Friday, February 5, 2016

Why You're Still Paying Fuel Surcharges After the Oil Crash (BusinessWeek)

Zombie fuel fees maintain a grip on airlines and other companies.

The collapsing price of oil that has upended the global economy has also caused understandable rejoicing at transportation companies, where big savings from cheap fuel will inevitably show up in the bottom line. Yet many of the surcharges that truckers, railroads, and—especially—airlines tacked on during the years of expensive oil have proven resilient. Travelers and other customers are still paying these zombie fuel fees even now, with crude at $32 per barrel.

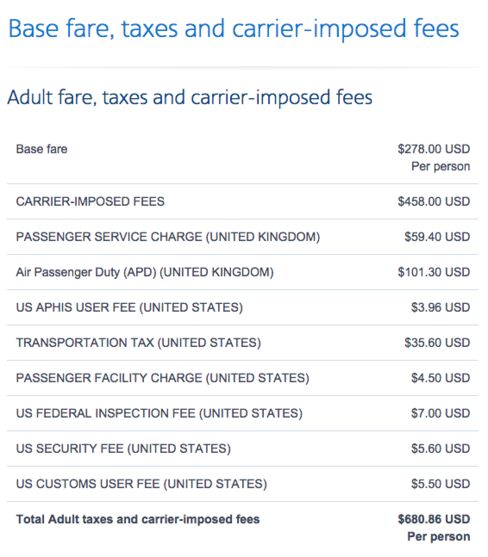

Here are the fare, taxes, and surcharges from a randomly selected American Airlines flight from Los Angeles to London in February. You won’t see anything labeled “fuel surcharge,” but that doesn’t mean you’re not paying an extra fee held over from the days when crude sold for more than $100 per barrel.

Unlike their peers in rail and trucking, U.S. airlines retired the term “fuel surcharge” in response to a 2012 ruling from the U.S. Department of Transportation that required carriers to demonstrate some relationship between a fuel-related fee and the price of fuel. Few airlines wanted to shed the surcharge, however, so international air travelers now pay hundreds of dollars in “carrier-imposed fees” or “carrier fees” instead. Airline ticketing software groups these fees under the designation “YR,” a catch-all category that can cover a fuel surcharge, insurance, and whatever else an airline sees fit to tack on to the base fare. Airlines don’t have these surcharges on domestic itineraries.

“The airlines have been very careful to shroud everything in as much mystery as possible,” says Charles Leocha, founder of Travelers United, a consumer-advocacy group.

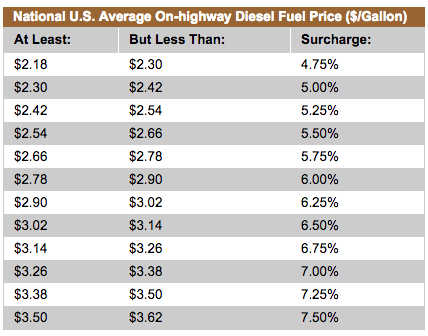

Only cruise lines have abolished fuel surcharges as energy costs have dropped off precipitously. Airlines, major trucking companies, shippers such as FedEx and UPS, and railroads all continue to assess fuel surcharges in the normal course of business. The cargo haulers tend to publish tables of their surcharges, which are pegged to market prices. Here’s one from UPS for ground shipments:

Current fuel surcharge schedule for UPS ground shipments.

UPS

The monthly rates at both FedEx and UPS have steadily dropped, as in the table above, falling in tandem with fuel costs. UPS has a 4.25 percent surcharge for air shipments, down from 16 percent in July 2011, according to BirdDog Solutions, a Hickory, N.C.-based shipping consultant. Over the past year, UPS and FedEx surcharges for air cargo have dropped 2.8 percent and 2.3 percent, respectively, the firm said.

Airlines don’t publish similar surcharge schedules, and the vagueness serves an important purpose: Many big-volume corporate travel buyers get their airline discount applied to base fares, while surcharges are paid in full. The passenger airline surcharges have averaged about $450 round-trip on trans-Atlantic itineraries for about three years and fluctuate very little, said Rick Seaney, chief executive of FareCompare.com, which monitors the data monthly. Surcharges to Asia and South America average between $420 and $440. On some international tickets, Seaney said, the surcharges cost more than the base fare.

“The whole thing is crazy, really,” says Bob Harrell, who runs a consulting firm that tracks airfares. “It started out as something that made sense, but it’s morphed into something that doesn’t make sense. After [airlines] got the fares up, they didn’t want to bring them down.”

That’s because the surcharges are an important part of airlines’ profitability. These fees “reflect a variety of factors and market forces that vary from market to market,” said Vaughn Jennings, a spokesman for Airlines for America, which represents most of the large U.S. carriers. “Airline pricing decisions and how prices are constructed are made individually by carriers in the highly competitive market for air transportation.” Moreover, Jennings said, these charges are included in the total price consumers see before they purchase.

The American way of handling surcharges isn't mirrored in other markets. Airlines in Japan—which regulates surcharges—and South Korea have begun abandoning these fees in recent weeks. Australia’s Qantas began rolling them into base fares a year ago. Hong Kong's Civil Aviation Department has banned fuel surcharges for flights originating there effective Feb. 1 because fuel prices have “greatly reduced and stabilized to a reasonable level,” the agency said.

The drop in fuel expenses also presents a financial issue for airlines keen to retain fuel surcharges as a way to bolster income. On Delta Air Lines’ recent quarterly earnings call, an analyst questioned how close the airline is to the lower edge of fuel surcharges in Japan. “In the past we’ve been able to roll those surcharges into the base fares as they changed, but I'm not predicting what the future is, nor do we want to comment on how we think that will roll out in the future,” replied Glen Hauenstein, Delta’s chief revenue officer. On its website, meanwhile, Delta notes the fees can total as much as $650 each way.

The high price of surcharges has embarrassed airlines in the past. In 2013, for instance, American apologized to some customers after applying fuel surcharges as high as $700 to some tickets issued with award miles. But that hasn't prompted the carriers to rethink the reliance on these fees. While lower fuel costs have provided a huge windfall in the transportation sector, many companies have been caught on the wrong side of expensive fuel hedging contracts. For example, Delta, Southwest, and United booked combined losses north of $1 billion last year for having locked in fuel at above-market prices. (The largest airline, American, does not hedge fuel.) Along with cheaper spot fuel prices, surcharges help lessen the sting of hedge losses and provide a backstop should prices spike.

Most truck carriers likewise have a wide range of surcharges and negotiate each of these with their customers individually, said Sean McNally, a spokesman for the American Trucking Associations. Most trucking companies and railroads consider fuel surcharges a form of insurance, according to Lee Klaskow, a Bloomberg Intelligence rail and trucking analyst. It's just another way to hedge against the cost of fuel. “For trucking,” Klaskow said, “if you say the rate is this and a component of that rate is going to float to the price of fuel, then you’re pretty much covering your tush.”

Subscribe to:

Posts (Atom)