Investors who’ve made a fortune in the country say that with oil's plunge, the ruble's collapse, and Putin in power, all bets are off

For a decade, Dmitri Barinov has been following the volatile economy of his homeland from the safe distance of Union Investment’s offices in Frankfurt. Last year, as other money managers were steering clear of Russia’s broken economy, the Moscow-born Barinov pulled off something of a coup: He persuaded his bosses to take the plunge and buy Russian government bonds. It was a narrow bet, but he ended up winning because the central bank—after implementing the biggest interest rate hike since the Russian financial crisis in 1998 to prop up the collapsing ruble—changed course and aggressively backtracked. In the first 10 months of 2015, ruble-denominated government bonds handed investors such as Barinov a 25 percent return in dollar terms, the biggest gain for local bonds anywhere.

This year not even Barinov can spot an escape from the rubble of an economy mired in its longest recession in two decades. Sanctions imposed by the U.S. and the European Union to punish President Vladimir Putin for meddling in Ukraine remain a drag on growth. And oil’s decline to a 13-year low has been catastrophic for Russia, where almost 50 percent of government revenue comes from crude and natural gas. “With oil, you rely on a very volatile factor,” says Barinov, who oversees about $2.6 billion in assets. So as far as he’s concerned, “all bets are off.”

A persistent glut in crude supply could push prices to as low as $16 a barrel this year, according to former Russian Finance Minister Alexei Kudrin. Kudrin won plaudits overseas for his stewardship of Russia’s finances during Putin’s first decade in power. As the current crisis deepened, Bloomberg News reported in December, he was in discussions about a possible return to government. (He declined to comment on that.) A Putin ally, Kudrin remains negative about Russia’s prospects. “Over the next year to 18 months,” he says, “Russia will suffer major economic difficulties.”

Thanks to the plunge in oil prices, says Dmitri Barinov, "all bets are off" when it comes to investing in Russia.

In his early days in office, Putin didn’t have to contend with such unpleasantness. The year he came to power—2000—oil traded at an average of $28.44 a barrel. For eight years, he benefited from rising oil revenue and gross domestic product growth averaging 7 percent. Putin usually revels in his annual yearend press conference, fielding mostly harmless questions for hours on end. At the one on Dec. 17, however, even reporters from state-controlled media grilled him on the economy. Tamara Shornikova, a journalist from a state TV channel, asked the 63-year-old Putin how pensioners and others can get by when “bills keep growing.”

The president, his mood clearly darkening, noted disparagingly that the channel’s “audience is not very large, probably, but I sometimes watch your programs.” He said the government was trying to index pension increases to inflation (12.9 percent last year). “We will see how the situation in the Russian economy plays out,” he said. “I would really like 2016 indexation to be at least on par with the annual rate of inflation. I cannot say whether we will be able to do it or not.”

With the 2015 budget based on $50 a barrel, says former Deputy Economy Minister Mikhail Dmitriev, “even $40 a barrel is a dangerous scenario for Russia.” The country holds parliamentary polls in September and a presidential election in 2018, when Putin is expected to run again. The election cycle puts pressure on the government to spend beyond its means, says Dmitriev, who five years ago accurately foresaw the street demonstrations over allegations of vote rigging in legislative elections that turned into the biggest protests of Putin’s rule. “If social dissatisfaction boils over,” he says, “Russia will adopt a populist economic policy for an extended time.”

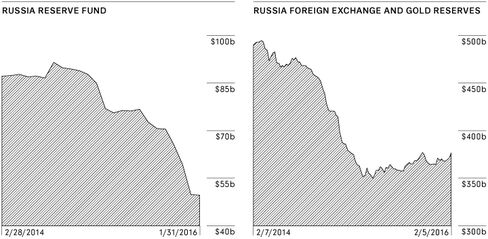

That kind of spending could exhaust Russia’s National Wellbeing and Reserve funds—currently totaling about $120 billion—within a year or two, says former Russian government adviser Sergei Guriev, who takes over as chief economist of the European Bank for Reconstruction and Development in mid-2016. “After that,” he says, “they will have to increase taxes on businesses, which will undermine incentives to invest, resulting in continuing capital outflow and a further decline in GDP.”

In mid-January, as snow blanketed Moscow, the mood was grim at the Gaidar Forum, a kind of Russia-focused mini-Davos. The yearly economic conference is named after the free-market Russian economist Yegor Gaidar, who pioneered the shock therapy that introduced capitalism to Russia in the early 1990s. Finance Minister Anton Siluanov set the tone for the event, warning that without deep budget cuts to keep the deficit at 3 percent, the country risks a financial crash like that of the late ’90s, when Russia defaulted on its debts, the ruble crashed, and inflation spun out of control.

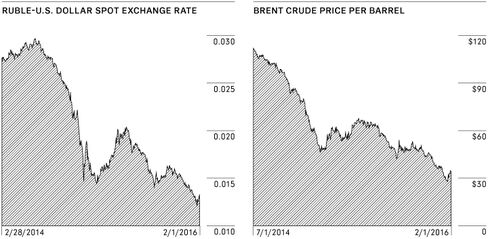

Siluanov’s assessment surprised no one. Russian GDP contracted 3.7 percent last year and could fall as much as 3 percent in 2016 if oil prices average $35, according to the central bank. In January, the ruble sank to new depths—60 percent below its value against the dollar in mid-2014.

On a weekday evening in January at Moscow Domodedovo Airport, a trickle of passengers flowed through passport control, with half the booths closed. Several carriers, including Delta Air Lines, Air Berlin, and Cathay Pacific Airways, have stopped flying to Russia because of low passenger traffic and the ruble’s devaluation.

Last December, in the runup to New Year’s Eve and Orthodox Christmas festivities, retail sales—which fueled profits for the German cash-and-carry chain Metro, Sweden’s Ikea, and others during the boom years—had their biggest contraction since 1999. Not long ago, the Russian car market was set to overtake Germany’s, the largest in Europe. Yet in 2016, auto sales are expected to fall for a fourth consecutive year.

Putin has said Ukraine-related sanctions have helped devastate the Russian economy. He sees them as a conspiracy against Russian resurgence on the world scene. But the impact of sanctions pales in comparison with that of oil. In a recent report, Citigroup said sanctions are responsible for just one-tenth of Russia’s economic contraction, with plunging crude prices responsible for the rest.

Union Investment’s Barinov is hardly alone in scaling back investment in Russia. After also reaping profits from bond gains last year, Ogeday Topcular, managing partner at Ram Capital in Geneva, who helps oversee $300 million in fixed-income assets, sold all of his Russian local debt holdings in mid-2015 because of concern about the ruble’s dependence on oil. Mark Mobius, chairman of the emerging-markets group at Franklin Templeton Investments, which last year shut its underperforming 20-year-old Russia fund, says the oil curse is weighing heavily on the economy. “In view of the fact that the Russian government budget has been so reliant on oil prices, it is clear that the prospects for the economy and the market aren’t good,” he says.

Russia may exhaust its $120 billion in rainy-day funds within a year or two, says one former government adviser

Last fall, a glimmer of hope pierced the gloom. Russian assets rallied following the start of Putin’s air war in support of Syria’s President Bashar al-Assad in September. It was a clever-looking ploy by Putin, who has a knack for outflanking Western leaders. The idea was that Russian intervention would give Moscow a role in high-level diplomatic efforts to find a resolution to the Syrian civil war—and a seat at the top table of world powers once again.

If only temporarily, the gambit worked. Putin’s intervention forced U.S. and European leaders to engage in a conversation with Russia, fueling speculation that Ukraine-related sanctions might be eased. “Of course Putin wants to get out of isolation,” says Gleb Pavlovsky, a political analyst who advised the Kremlin during Putin’s first two terms. “The Syrian campaign was dreamed up precisely as a way to get out of isolation.”

At the end of last year, the U.S., Russia, and other big players agreed to push for a power-sharing government in Damascus by the middle of this year and elections a year later. In February they came up with a cease-fire plan. But the outcome of the peace process was in doubt as a Kremlin-backed military offensive not only shored up the Assad regime but also dangerously poisoned relations with Turkey, a NATO member and one of Russia’s biggest trading partners, which threatened to send troops to Syria.

Putin’s failure to diversify the economy away from its heavy dependence on oil remains the country’s fatal flaw. “The Russian government missed opportunities to implement serious reforms in the economy and diversify the budget revenues,” says Marco Ruijer, who oversees about $7 billion of debt as a money manager at NN Investment Partners in The Hague. While some Russian sovereign and corporate bonds are “attractive,” he says, “many investors are now selling everything that’s oil-related, and Russia is part of that, of course.”

Cayman Islands-based Prosperity Capital Management, which has $2 billion invested in the country, is a rare bull among bears. It’s counting on a rebound in oil prices and an improvement in the geopolitical climate. “The issue of sanctions has been pushed aside,” Prosperity director Ivan Mazalov says. “Investors are used to working with Russian assets in the new reality.” In this new reality, if there’s any ray of hope, it’s that the markets have already discounted Russia’s myriad problems, says John Manley, who helps oversee about $233 billion as chief equity strategist for Wells Fargo Funds Management in New York.

Putin could reassure investors by moving ahead with long-stalled privatization plans as well as improving the rule of law to ease pressure on businesses, says Ivan Tchakarov, chief economist in Russia for Citigroup. Russia ranked 119th on Berlin-based Transparency International’s corruption perception index, released in January, behind Pakistan and Tanzania.

Fundamentally, Russia is a “commodity play,” says Gary Greenberg, who helps oversee about $1.8 billion as head of emerging-markets equities at London-based fund manager Hermes Investment Management. Since Russia’s main exports—raw materials—are dependent directly and indirectly on China’s lackluster growth, the outlook for Russia “is moderate at best,” he says.

“In terms of emerging markets, it feels a lot like 1997,” says John-Paul Smith, the former Deutsche Bank strategist who predicted Russia’s 1998 market crash and went on to found Ecstrat, a London-based research firm. “The Chinese have been doing everything to get their economy going again, and they simply can’t do it.”

Then there’s the bleak view of Bill Browder, an American investor who became one of Putin’s most nettlesome bêtes noires and paid a price for it. Browder, a grandson of a U.S. Communist Party leader, ventured into Russia in the 1990s. He made a fortune specializing in undervalued Russian blue-chip stocks such as state-run Gazprom, the largest gas producer in the world, which saw the value of its stock soar 750 percent from 1999 to 2005. Browder’s Hermitage Capital Management started with $25 million in 1996 and at its 2005 peak had $4.5 billion under management, making it the biggest investment fund in Russia.

The London-based Browder was barred from Russia in 2005 after pushing aggressively for the rights of minority shareholders. He became a vocal critic of Putin after his accountant, Sergei Magnitsky, uncovered the theft of $230 million from the Russian treasury and later died under suspicious circumstances in a Moscow prison in 2009. For Browder, like many investors with long experience in Russia, it all comes down to Putin, who’s expected to win reelection to another six-year term in 2018, despite Russia’s economic travails. “No matter how cheap anything might seem,” Browder says, “it doesn’t matter if you’re on a negative trajectory.” He says the economy still has depths to plumb. “It hasn’t hit bottom, because Putin is still in power.”

No comments:

Post a Comment