On Wall Street, the still-essential business of banking will go on—but maybe without as many suits.

Are the humans of finance an endangered species?

People are still the lubricant that oils the wheels of finance, toiling at innumerable tasks—executing and settling trades, writing analysis, monitoring risk. That’s about to change.

Squeezed by low interest rates, shrinking trading revenue, and nimbler technology-based competitors, banks are racing to remake themselves as digital companies to cut costs and better serve clients. In other words, they’re preparing for the day that machines made by men and women take over more of what used to be the sole province of humans: knowledge work. Call it self-disruption.

Consider venerable State Street, a 224-year-old custody bank that predates the steam locomotive and caters to institutional investors such as pensions and mutual funds. In February, State Street executives told analysts that after spending five years upgrading technology systems, they realized how much more could be done. “We have 20,000 manual interventions on trades every day,” said Michael Rogers, president of the Boston bank. “There’s a huge opportunity to digitize that and move it forward electronically.”

But one person’s opportunity is another person’s exit package. State Street had 32,356 people on the payroll last year. About one of every five will be automated out of a job by 2020, according to Rogers. What the bank is doing presages broader changes about to sweep across the industry. A report in March by Citigroup, the fourth-biggest U.S. bank, said that more than 1.8 million U.S. and European bank workers could lose their jobs within 10 years.

Advances in cloud-based computing and algorithms capable of combing vast amounts of data for decision-aiding patterns make this possible. The human brain is a wondrous machine, but it isn’t changing. The pace of technological advancement is accelerating, and artificial intelligence (AI) may one day make many forms of work extinct. It’s a topic that’s dominated forums such as the Milken Institute Global Conference in May and has spurred talk of government-funded universal basic income programs that would pay citizens a regular stipend.

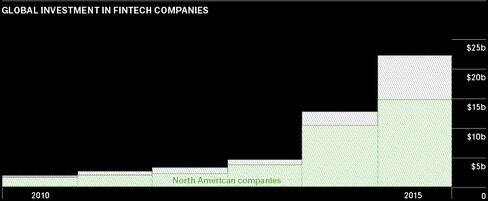

All of that’s a ways off. What concerns bankers today—the ones who’ve survived round after round of post-financial crisis job cuts—is how humans will coexist with machines over the next few decades. Maligned in recent popular culture via movies like The Big Short, the still-essential business of banking isn’t getting a breather after new regulations reined in profits and risk-taking. It’s under assault from all sides by fintech startups devising new ways of doing old kinds of banking. From Hong Kong to Dublin, Brooklyn to Dubai, these upstarts attracted $22.3 billion in funding last year, up 75 percent from 2014, according to an Accenture analysis of data from research firm CB Insights.

Bank executives know what’s coming. So they’re setting up coder labs and investing in startups, teaming up with digital competitors or buying them outright. JPMorgan Chase, the biggest U.S. lender by assets, is using AI to identify potential equity clients. And it’s marshaling OnDeck Capital’s client-vetting algorithm to speed lending to small businesses. Both Bank of America and Morgan Stanley, which together employ more than 32,000 human financial advisers, are developing automated robo-advisers. More than 40 global banks have joined forces with startup R3 to develop standards to use blockchain, software that allows assets to be managed and recorded through a distributed ledger, to overhaul how assets are tracked and transferred.

The universal theme of banking’s tech strategy is to make sure that, internally and in dealing with clients, ones and zeros flow seamlessly without messy human interference. At State Street, for example, incompatible systems and a variety of inputs mean people need to manually work an order— some 50,000 of them arrive each month in the form of a telephonically transmitted document that many assume had gone the way of the cassette tape: the fax. Instructions received that way require a human to manually shuttle trade and settlement information between screens. In other instances, missing or mismatched information in complicated trades needs to be reconciled by a person.

Machine learning, where the decision-making power of algorithms improves as more data are raked in, can replace people in some instances, say finance executives including Daniel Pinto, head of JPMorgan’s investment and corporate bank. Algorithms already tackle tasks such as vetting banking clients, pricing assets, and hedging some orders without human intervention. “As we make those processes more and more efficient, you will need less people to do what we do today,” Pinto says.

Beyond that, bots armed with AI and the ability to understand and respond in natural language can be used to answer clients’ queries and eventually execute transactions, says Suresh Kumar, chief information officer of Bank of New York Mellon. “You start with something simple, maybe just offering information, then you start doing transactions,” Kumar says. “We obviously want to automate everything, but you have to prioritize.”

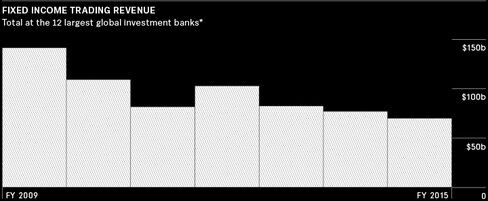

Even those at the top of the industry’s hierarchy aren’t immune. Bond trading is the single biggest source of Wall Street profit. It’s also something of a broken market. Post-crisis regulations have crimped banks’ ability to stockpile bonds, changing their traditional role in markets and creating an opening for dozens of electronic-trading startups looking to connect buyers and sellers. Fixed-income trading at the world’s biggest investment banks brought in $70 billion last year, half the 2009 level, according to data compiled by financial research firm Coalition.

When investors embrace electronic trading, margins collapse while volumes, for a few winners, surge. In equities, electronic trading has decimated the number of salespeople, traders, and floor brokers; it’s also ushered in high-speed trading firms and alternative exchanges like dark pools. These changes are well under way in government bond trading, where technology-powered firms such as Citadel Securities have made inroads, and in foreign exchange, where year-old XTX Markets now ranks as one of the world’s biggest FX firms.

In the $8.16 trillion corporate debt market—the last big refuge for people who trade over the phone—electronic trading of investment-grade bonds grew 25 percent last year, according to Greenwich Associates. MarketAxess, which is one of the biggest electronic venues in credit, clocked a 27 percent surge in trading volume in the first quarter. (Bloomberg LP, the parent company of Bloomberg News, competes with MarketAxess in providing a venue for electronic trading of corporate debt.) Other upstarts, typically founded by Wall Street refugees, have jumped in.

As with other threats, such as e-payments and automated investing, established players aren’t sitting still. They’re opening up electronic venues so institutional clients—who use investment banks for a bundled array of services—have less reason to wander. Goldman Sachs is offering clients access to its proprietary research and analytical tools through web platforms to entice them to do more business with the firm. As banks automate fixed-income trading operations, “they will start making drastic decisions about their trading personnel,” says George Kuznetsov, Coalition’s head of research and analytics.

Even in investment banking, where the human element is central to dealmaking, technology will have an impact. Many parts of the initial public offering process are “ripe for workflow automation,” Goldman Sachs CIO Martin Chavez said in September.

What all of this means is that the number of front-office trading and dealmaking jobs has been in decline since 2007, just before the financial crisis, when it peaked at 64,521. It was 14 percent lower last year at the world’s largest investment banks, according to Coalition. Even if revenues recover because of higher interest rates, improving economies, and a rebound in debt trading, new platforms will simply scale up to the higher volumes without needing many more flesh-and-blood operators. Wall Street has reached peak human.

Saying that an industry is contracting doesn’t mean people won’t be earning a living in finance down the road. Banks will need computer engineers and data scientists—and old-fashioned voice traders to make markets in more bespoke assets such as structured credit. People will be needed to conceive of, create, and maintain new products. Matthew Dixon, an assistant professor of finance at the Illinois Institute of Technology who has studied machine learning, tells aspiring traders to learn computer programming. “The days you could just learn Excel and do some fundamental analysis are over,” Dixon says. “You’re going to be working with larger and larger amounts of data, and you’ll need to know how to use algorithms.”

Wall Street will go on—but maybe without as many suits.

No comments:

Post a Comment